If you’re feeling like the weight of your debts is holding you down, don’t worry; you are not alone. Millions of people around the world live in debt, but there are several steps you can take to get out of debt faster and for less money than ever before.

This step-by-step guide on ”how to get out of debt fast on your own” will help you identify the source of your debt and then figure out how to pay it back in full without doing too much damage to your financial prospects.

The sooner you start, the better!

Getting out of debt is rough. I’m not going to sugarcoat it. It’s an uphill battle. It’s more than just changing some numbers on paper. It takes a whole shift in your mindset. You can get out of debt quickly on your own.

Decide if you really want to get out of debts

That may seem kind of silly. Why would you be looking for ways to get out of debt if you really didn’t want to get out of debt?

What I mean by this is that it takes more than just flippantly saying, “Oh, sure. I’d like to pay off some debt.” There’s a lot more to it than that.

To get out of debt you’re going to have to make some cuts that probably won’t be fun. You’re probably going to have to learn to say no when your friends want to go shopping or when your buddies want to take a road trip to some big game.

Most people (myself included) end up in debt because we live above our means. Sometimes it’s small stuff like eating out for lunch every day. Or it may be something big like a vacation or a new TV that you don’t have the money for.

Credit cards are one of the best tools of the debt devil. They make it easy to impulse buy and worry about the consequences later.

To get out of debt you’re going to have to have a change in mindset.

Also Read: Best Loan Apps in Nigeria That Don’t Require BVN

Set Up A Budget

This is another dirty word for some people: B-B-Budgets. My wife was so against this when I first started campaigning to put our family on a budget.

A lot of people see a budget as a financial prison. They think that within a budget, you are no longer free to spend your money as you, please. You’re caged in, limited, and imprisoned.

I have come to find that a budget is one of the most financially freeing things in the world.

Wild talk, you say!?

Let me tell you why I love budgets. Budgets free you from worrying about your finances. Budgets allow you to allocate your money before it is ever spent.

In a budget, you can look at the month and know there will be enough money to pay for everything. On a budget, you can feel guilt-free when you go out to dinner or buy a pair of shoes or tickets to the game.

Why? Because when your money has been allocated before it hits your wallet, you know exactly how much you can spend on things.

Check out my post here on how to set up a budget.

Once you have your budget, you should have a good idea of where your finances stand. If you were honest in looking at where your money goes you probably found that you were spending more than what you brought in.

Find A Way to Make Expenses Less Than Income

Oh boy. Here comes the painful part. You have to find a way to spend less than what you bring in each month.

This seems simple, but I’ll say it anyway: you have to find extra money somewhere to be able to pay off debt. The most straightforward way to do it is to cut expenses.

The target I like to shoot for is $200 per month. For some people, that may be easy. Great! Then cut more, and your debt will go down faster. For some, the only way they could find an extra $200 is to quit eating or have their electricity cut off. That’s ok. Cut as much as you can.

Where do you find this $200 in your budget? See if you’re spending money on any of this:

- Cable: $100+ /month

- Eating out at lunch – $6–$10 a day.

- Starbucks: $5 a pop. It doesn’t take many trips to add up.

- iPhone, Android, – $40+ /month more than a basic cell phone

- Home phone in addition to a cell phone: $30/month

This isn’t even getting into things like cutting out some of the more expensive items at the grocery store, evaluating your driving habits that use more gas, setting your thermostat a little higher in the summer or lower in the winter, and dozens of other money-saving ideas.

If you look, I’d bet it’s not hard to find an extra $200 in your budget. It may not be fun to cut cable, but if you want to get out of debt badly enough enough, do it.

Also Read: 5 Apps to Help You Save Money in Nigeria

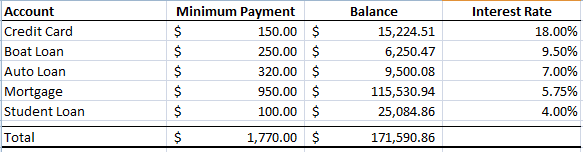

Outline All Your Debts

With the money allocated to pay down your debt, you need a list of everything you want to pay off.

Pull out the last statements from all of your credit cards, your mortgage, auto loans, student loans, lines of credit, and any other debt you have. Make a list of the minimum payment, current balance, and interest rate of each account.

I prefer to put all of this in Excel since it makes sorting your list much easier. If you don’t have Excel, Google Docs works just as well. A plain old notebook works fine too.

When you’re done you should have something that looks like this:

Apply The Extra To The Highest Interest Rate

Here is where the rubber meets the road. You have your debt reduction plan. All you have to do is follow it.

Take the extra $200 from above and put it towards the debt with the highest interest rate. This should be in addition to the minimum payment.

So using the example above I would start paying $350 each month on my credit card. I would keep paying this amount each month until it was totally paid off.

Once the credit card is paid off I would put the $350 that was going toward the credit card into the boat loan. So the total payment was $600.

Once the boat was paid off, the extra $600 would go towards the auto loan so I would be paying $920 a month.

With the car paid off, I would add the $820 a month to my mortgage so I was paying $1,870 per month.

Finally, with the mortgage paid off, I could put $1,970 toward my student loans.

By doing this I would be debt-free in less than 10 years and save over $52,000 in interest! 10 years may sound like a long time, but don’t forget you’re paying your mortgage off too. If you didn’t want to pay off your mortgage you could cut several years out of that timeline.

That’s pretty powerful to be able to pay off over $170,000 in debt in such a short time! Could you imagine being totally debt-free? You would have an extra $2,000 per month in your pocket!

Also Read: Is It Safe to Keep Money in a Safe Deposit Box?

Don’t Charge Up More Debts

Here is a big key that so many people miss. Working to get out of debt is great, but if you just charge everything back up again, it totally defeats the point.

Don’t expect this to happen by chance. You need a plan to make sure you don’t get back into debt. That may mean you cut up your credit cards. Maybe you just need to put them in an inaccessible place, such as a safe deposit box.

It’s also a good idea to identify your weak points. If you can’t resist the home shopping channel, then make sure you never watch it. If a shiny new car makes your mouth drool, then don’t drive by any car dealerships!